On-Demand Drone Insurance vs Annual Plans: Which Is Better for You?

If you’re trying to choose between on demand drone insurance and an annual policy, you’re not alone. This is one of the most common decisions drone pilots face—especially beginners and part-time flyers.

Table Of Content

- On-Demand Drone Insurance vs Annual Plans: Which Is Better for You?

- What Is On-Demand Drone Insurance?

- What Is Annual Drone Insurance?

- Why Choosing the Right Insurance Type Matters

- Beginner Understanding: Which One Should You Start With?

- On-Demand vs Annual Drone Insurance – Detailed Comparison, Costs, and Use Cases

- On-Demand vs Annual Drone Insurance: Side-by-Side Comparison

- Cost Breakdown: Which One Is Actually Cheaper?

- Real-World Use Cases: Which One Fits Your Situation?

- Coverage Features: What Do You Actually Get?

- FAA Rules and Insurance: What You Should Know

- Smart Decision Guide, Common Mistakes, and Final Verdict

- Common Mistakes to Avoid

- Risk vs Convenience: The Real Trade-Off

- Smart Decision Framework (Quick Guide)

- Advanced Tip: Hybrid Strategy

- Final Verdict: Which One Is Better?

- FAQs: On-Demand vs Annual Drone Insurance

- What is on demand drone insurance?

- Is hourly drone insurance worth it?

- When should I choose annual drone insurance?

- Can I switch from on-demand to annual insurance?

- Does on-demand insurance include liability coverage?

- What happens if I forget to activate on-demand insurance?

- Is annual drone insurance cheaper in the long run?

On one hand, hourly or pay-per-flight insurance sounds flexible and cost-effective. On the other, annual coverage offers consistent protection without needing to think before every flight.

So which one actually makes sense for you?

This guide breaks it down in a simple, practical way—so you can choose the right option based on how you fly, not just what sounds cheaper.

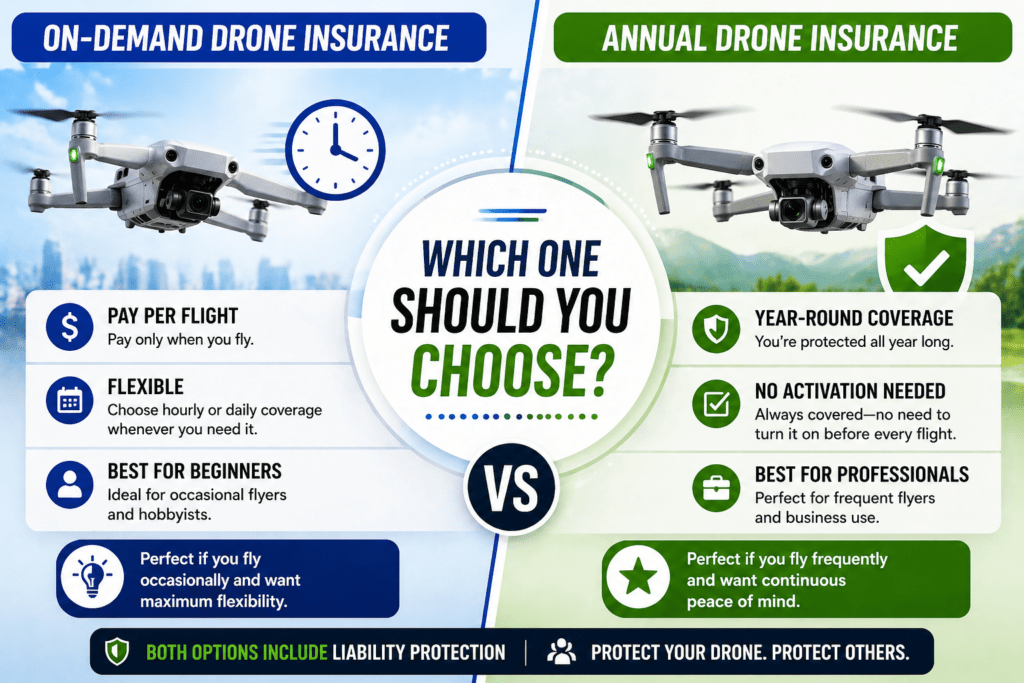

What Is On-Demand Drone Insurance?

On demand drone insurance (also called hourly drone insurance or pay per flight insurance) is a flexible coverage model where you only pay when you actually fly your drone.

Instead of paying for a full year, you activate insurance for a specific time—usually by the hour, day, or project.

This type of insurance is popular among:

- Beginners who don’t fly regularly

- Freelancers with occasional projects

- Hobbyists testing different locations

Here’s why it matters: you avoid paying for coverage when your drone is sitting at home.

What Is Annual Drone Insurance?

Annual drone insurance is a traditional policy where you pay a fixed yearly fee for continuous coverage.

This means your drone is insured at all times—whether you’re flying once a week or every day.

Annual plans are typically used by:

- Frequent drone users

- Content creators and professionals

- Commercial operators under Part 107

If you’re planning to use your drone for work, you’ll likely move toward annual coverage sooner or later.

Why Choosing the Right Insurance Type Matters

This decision isn’t just about cost—it’s about how you manage risk.

Imagine this:

You forget to activate your hourly insurance before a flight. Something goes wrong. Now you’re fully responsible for the damage.

Or the opposite:

You pay for a full-year policy but only fly once a month. You’re overpaying for coverage you barely use.

Here’s why it matters: the wrong choice can either expose you to risk—or waste your budget.

Beginner Understanding: Which One Should You Start With?

If you’re new to drones, your flying habits are still unpredictable. That’s why many beginners start with on demand drone insurance.

It gives you flexibility without long-term commitment. You can test how often you fly and upgrade later.

However, if you already know you’ll be flying frequently—especially in public spaces—annual coverage may actually save you money and effort.

To understand how drone insurance works in general, you can explore this full guide: Drone Insurance Guide 2026

And if you want to compare insurance with manufacturer protection plans, this breakdown helps: Drone Insurance vs DJI Care

Now that you understand the basics, the next step is to compare both options in detail—costs, use cases, pros, and real-world scenarios.

On-Demand vs Annual Drone Insurance – Detailed Comparison, Costs, and Use Cases

Now that you understand the basics of on demand drone insurance, let’s go deeper. This is where the real decision happens—comparing both options based on cost, flexibility, and real-world usage.

The goal isn’t to find the “cheapest” option. It’s to find what actually fits how you fly.

On-Demand vs Annual Drone Insurance: Side-by-Side Comparison

Let’s break this down in a simple way.

- Flexibility

On-demand insurance wins. You activate coverage only when needed. - Convenience

Annual insurance wins. No need to think before each flight. - Cost Control

On-demand is cheaper for occasional users. - Long-Term Value

Annual plans are better for frequent flyers. - Risk of Forgetting Coverage

Higher with on-demand. Zero with annual.

Here’s the key takeaway: on-demand insurance gives control, while annual insurance gives consistency.

Cost Breakdown: Which One Is Actually Cheaper?

At first glance, hourly drone insurance looks cheaper. But the real answer depends on how often you fly.

Typical pricing in the USA:

- On-demand insurance: $5–$15 per hour or $10–$50 per day

- Annual insurance: $150–$500+ per year

Now let’s make it practical.

If you fly once or twice a month, on-demand is usually cheaper.

If you fly every week—or multiple times a week—annual coverage becomes more cost-effective.

For a deeper cost analysis, check this full breakdown: Drone Insurance Cost 2026

Real-World Use Cases: Which One Fits Your Situation?

Instead of guessing, let’s match each option to real-world scenarios.

Use Case 1: Beginner Pilot

You’re still learning and don’t fly regularly. On-demand insurance makes more sense because you only pay when you practice.

Use Case 2: Hobbyist Photographer

You fly on weekends for fun or content. Depending on frequency, you can start with on-demand and switch later.

Use Case 3: Freelance Drone Operator

You take occasional paid projects. On-demand insurance is ideal for project-based work.

Use Case 4: Full-Time Professional

You fly regularly for work. Annual insurance is the smarter choice for consistency and cost savings.

If you’re planning to turn your drone into a business, explore this guide: Drone Insurance for Business

Coverage Features: What Do You Actually Get?

Both on-demand and annual plans usually offer similar types of coverage—but the way you access them differs.

- Liability coverage – Protects against damage to others

- Drone damage (hull) – Covers your drone

- Coverage limits – Typically $500K to $1M

The difference isn’t in what you get—it’s in when and how you’re covered.

FAA Rules and Insurance: What You Should Know

In the USA, the FAA regulates how drones are flown—but not insurance.

You can review official guidelines here: FAA Drone Regulations

Here’s the important part: even though insurance isn’t legally required, you’re still fully responsible for any damage or injury caused by your drone.

That’s why choosing between pay per flight insurance and annual coverage isn’t just a financial decision—it’s a risk management decision.

Now that you’ve seen the detailed comparison, the final step is understanding expert tips, common mistakes, and how to make the best decision long-term.

Smart Decision Guide, Common Mistakes, and Final Verdict

By now, you understand how on demand drone insurance compares with annual plans. The final step is making a smart decision based on your real usage—not assumptions.

This section will help you avoid costly mistakes and choose the right path with confidence.

Common Mistakes to Avoid

Most drone users don’t choose the wrong insurance—they choose it for the wrong reasons. Here are the mistakes you should avoid.

- Choosing based on price alone

Cheap doesn’t always mean better. It depends on how often you fly. - Forgetting to activate on-demand coverage

This is one of the biggest risks. If you forget, you’re completely unprotected. - Overestimating how often you fly

Many beginners buy annual plans but rarely use them. - Ignoring liability coverage

Damage to others can be far more expensive than your drone itself.

Here’s why it matters: avoiding just one of these mistakes can save you hundreds—or even thousands—of dollars.

Risk vs Convenience: The Real Trade-Off

When deciding between hourly drone insurance and annual coverage, it comes down to one key trade-off.

On-demand insurance gives you flexibility and control—but requires discipline. You must remember to activate it every time you fly.

Annual insurance removes that risk. You’re always covered, but you pay more upfront.

Think of it this way:

- If you value flexibility → Go on-demand

- If you value peace of mind → Go annual

This simple mindset shift makes the decision much easier.

Smart Decision Framework (Quick Guide)

If you’re still unsure, use this quick decision framework.

- Fly less than 3–4 times a month → On-demand drone insurance

- Fly weekly or more → Annual drone insurance

- Do occasional paid projects → On-demand (per project)

- Run a full-time drone business → Annual coverage

This approach works for most users and keeps your costs aligned with your usage.

Advanced Tip: Hybrid Strategy

Here’s something many experienced drone pilots do—but beginners often overlook.

They use a hybrid approach.

For example:

- Start with on-demand insurance while learning

- Switch to annual coverage as flying becomes consistent

- Use on-demand for special high-risk projects (even if you have annual coverage)

This gives you both flexibility and long-term protection.

Final Verdict: Which One Is Better?

So, which is better—on demand drone insurance or annual coverage?

The honest answer is: it depends on how you fly.

There’s no universal winner. But there is a smarter choice for your situation.

If you’re a beginner or occasional user, on-demand insurance gives you flexibility without long-term commitment.

If you’re a regular or professional pilot, annual insurance provides better value and peace of mind.

In the end, the best insurance is the one you actually use—and rely on when it matters.

FAQs: On-Demand vs Annual Drone Insurance

What is on demand drone insurance?

It’s a flexible insurance option where you pay only when you fly, usually by the hour or per day.

Is hourly drone insurance worth it?

Yes, if you fly occasionally. It helps you avoid paying for coverage you don’t use.

When should I choose annual drone insurance?

If you fly regularly or use your drone professionally, annual coverage is usually more cost-effective.

Can I switch from on-demand to annual insurance?

Yes, many pilots start with on-demand and upgrade as their flying frequency increases.

Does on-demand insurance include liability coverage?

Yes, most plans include liability coverage, but limits may vary depending on the provider.

What happens if I forget to activate on-demand insurance?

You won’t be covered for that flight, and you’ll be responsible for any damage or loss.

Is annual drone insurance cheaper in the long run?

Yes, for frequent flyers, annual plans usually provide better value over time.

No Comment! Be the first one.