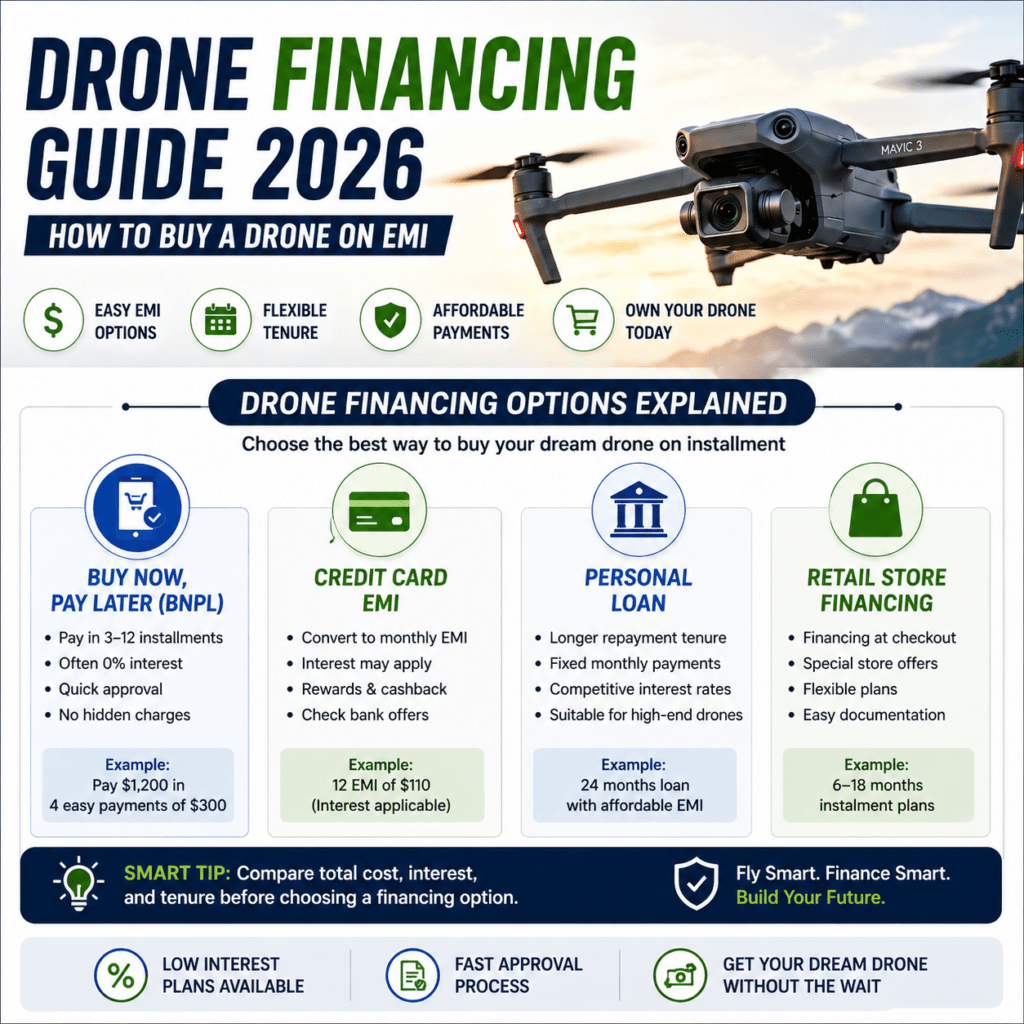

Drone Financing Guide 2026: How to Buy a Drone on EMI

Buying a high-quality drone isn’t cheap anymore. Whether you’re a beginner, content creator, or planning to start a drone business, the cost can easily go into hundreds or even thousands of dollars. That’s exactly where drone financing becomes useful.

Instead of paying the full price upfront, financing lets you spread the cost into manageable monthly payments. But here’s the problem—most people don’t understand how drone loans actually work, what options exist, or whether it’s even a smart decision.

This guide breaks everything down in a simple, practical way. By the end, you’ll know how to buy a drone on installment, which financing option fits your situation, and how to avoid costly mistakes.

What Is Drone Financing?

Drone financing is a way to purchase a drone by paying in installments instead of paying the full amount upfront. It works similar to financing a phone, laptop, or even a car—just on a smaller scale.

You choose a drone, select a financing plan, and then pay monthly installments (EMI) over a fixed period. Depending on the provider, you may also pay interest or fees.

Here’s the simple idea: you get the drone now, and pay for it over time.

Why Drone Financing Matters in 2026

Drone prices have increased as technology improves. Features like 4K video, obstacle avoidance, and long battery life make modern drones powerful—but also expensive.

This is especially important in the USA, where many users are turning drones into income sources—real estate photography, YouTube content, inspections, and more.

Here’s why financing matters:

- You don’t need a large upfront budget

- You can start earning with your drone immediately

- You can upgrade to better models instead of settling for cheap ones

If you’re still exploring which drone to buy, this guide can help you choose the right model: Drone Buying Guides

How Does Buying a Drone on Installment Work?

Buying a drone on installment is straightforward once you understand the process.

- Choose your drone

- Select a financing provider (store, bank, or app)

- Apply and get approved

- Pay monthly installments

Some plans offer 0% interest, while others charge a small percentage depending on your credit profile.

The key difference is flexibility—you don’t delay your purchase just because of budget limitations.

Beginner Understanding: Is Financing a Drone a Good Idea?

If you’re new to drones, financing can be both helpful and risky—depending on how you use it.

It makes sense if:

- You plan to use the drone regularly

- You want a better model for content or work

- You can comfortably afford monthly payments

It may not be ideal if:

- You’re unsure how often you’ll use the drone

- You’re buying just for occasional fun

- You’re stretching your budget too much

For beginners, it’s often smarter to start with a budget-friendly drone first: Best Budget Drones for Beginners

And if you’re planning long-term usage, especially for work, you should also consider protection and insurance: Drone Insurance Guide 2026

Now that you understand the basics of drone financing, the next step is to explore different financing options, costs, and which one actually fits your situation.

Drone Financing Options, Costs, and Real-World Use Cases

Now that you understand the basics of drone financing, let’s go deeper into how it actually works in the real world. This is where most buyers make mistakes—not because financing is bad, but because they choose the wrong option.

The key is simple: not all drone loans are the same. Some are flexible and low-cost, while others can quietly become expensive.

Types of Drone Financing Options

In 2026, there are several ways to buy a drone on installment. Each option has its own pros and trade-offs.

- Buy Now, Pay Later (BNPL)

Platforms like store financing or apps let you split payments into 3–12 months, sometimes with 0% interest. - Credit Card EMI

You can convert your purchase into monthly installments, but interest rates may apply. - Personal Loans

Banks or lenders offer fixed monthly payments over longer periods. - Retail Store Financing

Some drone sellers offer direct installment plans at checkout.

Each option works—but choosing the right one depends on your budget and how quickly you want to pay off the drone.

On-Demand vs Long-Term Financing: Which One Fits?

Just like insurance, financing also comes with short-term and long-term approaches.

Short-term (BNPL or 0% EMI):

Best if you can pay off the drone quickly without interest.

Long-term (loans or credit EMI):

Better for expensive drones but may include interest costs.

The key difference is total cost. A longer plan may feel affordable monthly—but you often pay more overall.

Real Cost of Drone Financing

Let’s break it down with a simple example.

Drone price: $1,200

- 0% EMI (6 months) → $200/month → Total: $1,200

- Loan (12 months, interest) → ~$110/month → Total: ~$1,320+

This shows something important: lower monthly payments often mean higher total cost.

Here’s why it matters—many buyers focus only on monthly affordability and ignore the total price they’ll end up paying.

Use Cases: Who Should Use Drone Financing?

Drone financing makes sense—but not for everyone. Let’s match it with real-world scenarios.

Beginner Hobbyist

If you’re just testing drones, financing may not be necessary. Start with a lower-cost drone first.

Content Creator (YouTube / Social Media)

Financing can help you access better camera drones that improve content quality.

Freelancer / Side Hustle

If you plan to earn from drone work, financing can help you start faster without waiting to save money.

Professional Drone Business

Financing is often a strategic investment—especially for high-end drones used in inspections, mapping, or filming.

If you’re planning to turn your drone into income, you should also understand insurance requirements: Drone Insurance Requirements USA

Key Factors to Consider Before Financing

Before you commit to any drone loan, consider these factors carefully.

- Interest rate – Is it really 0% or hidden in fees?

- Loan duration – Shorter is usually better

- Monthly affordability – Can you comfortably pay it?

- Total cost – What will you pay in the end?

This is where most buyers go wrong—they look at the monthly payment and ignore everything else.

Regulations and Responsible Drone Use

If you’re financing a drone in the USA, you should also be aware of FAA rules. These regulations apply regardless of how you purchased your drone.

You can review official guidelines here: FAA Drone Regulations

Why this matters: buying a drone on installment doesn’t change your legal responsibilities. You still need to follow airspace rules, registration requirements, and safety guidelines.

Now that you understand financing options, costs, and real-world use cases, the final step is learning how to make the smartest decision—and avoid common financial mistakes.

Smart Financing Strategy, Mistakes to Avoid, and Final Decision Guide

By now, you understand how drone financing works and what options are available. The final step is making a smart decision—one that helps you get the drone you want without creating financial pressure later.

This section focuses on practical strategies, common mistakes, and a clear decision framework you can follow.

Common Mistakes When Financing a Drone

Most people don’t run into problems because financing is bad—they run into problems because they overlook key details.

- Focusing only on monthly payments

A lower EMI feels comfortable, but it often increases the total cost. - Ignoring hidden fees

Processing fees, late charges, or interest terms can increase the final price. - Buying more than you need

It’s easy to finance a high-end drone, but not always necessary. - No backup plan for payments

If your income changes, monthly commitments can become stressful.

Here’s why it matters: one wrong decision can turn a useful investment into a long-term burden.

Smart Strategy: When Does Drone Financing Make Sense?

Drone financing works best when it supports a clear goal—not just a purchase.

It makes sense if:

- You plan to use the drone regularly

- You want to generate income (photography, videography, inspections)

- You can comfortably afford monthly payments

- You’re choosing a better drone that adds real value

It’s less ideal if you’re buying purely for occasional use or experimenting without a clear purpose.

If you’re still unsure about which drone suits your needs, this guide can help: Best Drones for Videos and Photos

Decision Guide: Should You Finance Your Drone?

Use this quick framework to decide:

- Beginner (learning phase) → Avoid financing, start budget-friendly

- Regular hobbyist → Consider short-term EMI (0% if possible)

- Freelancer / side income → Financing can accelerate growth

- Professional business → Financing becomes a strategic investment

This approach keeps your decision practical and aligned with your real usage.

Advanced Tip: Combine Financing with Protection

Here’s something many buyers overlook: when you finance a drone, you’re committing to monthly payments—whether the drone is working or not.

That’s why experienced users combine financing with protection.

For example:

- Financing covers the purchase

- Insurance covers risks like damage or accidents

This ensures you’re not stuck paying for a damaged drone.

If you want to explore insurance options, start here: Best Drone Insurance 2026

Final Verdict: Is Drone Financing Worth It?

So, is drone financing worth it?

Yes—if used wisely.

It’s a powerful tool that allows you to access better equipment, start earning earlier, and manage your budget more effectively.

But it’s not a shortcut. It requires planning, discipline, and a clear purpose.

The smartest approach is simple:

- Choose the right drone

- Select the right financing option

- Keep total cost in mind—not just monthly EMI

When done right, financing doesn’t just help you buy a drone—it helps you move forward faster.

FAQs: Drone Financing Guide 2026

What is drone financing?

Drone financing allows you to buy a drone on installment by paying monthly instead of upfront.

Can I buy a drone on EMI in the USA?

Yes, many platforms offer EMI or installment options through BNPL services, credit cards, or personal loans.

Is 0% drone financing really free?

Some plans are truly 0%, but others include hidden fees. Always check the total cost before committing.

Should beginners finance a drone?

Beginners should usually start with a budget drone before committing to financing.

What credit score is needed for drone loans?

It depends on the provider, but better credit scores usually get lower interest rates.

Is drone financing a good investment?

Yes, especially if you plan to use the drone for income or regular content creation.

Can I pay off my drone loan early?

Many lenders allow early repayment, but check for any prepayment penalties.