Drone Financing for Bad Credit in 2026 — Real Options That Actually Work

Drone financing for bad credit in 2026 is not a dead end — and I want you to hear that clearly before we go any further.

I’ve talked to a lot of people who gave up on buying a drone the moment they got rejected by one lender. That’s a mistake. The financing landscape in the USA has shifted significantly, and bad credit no longer automatically means no options.

What it does mean is that you need to know where to look, what to avoid, and how to approach drone financing for bad credit the smart way. That’s exactly what this guide covers.

Whether you’re buying a drone for a side hustle, a small business, or serious hobby use, there are real paths forward even if your credit score is not where you want it to be. I’ll walk you through every option available to USA buyers right now.

If you want a broader overview of how drone financing works before diving into the bad credit specifics, start with my drone financing guide 2026 — it gives you the full picture first.

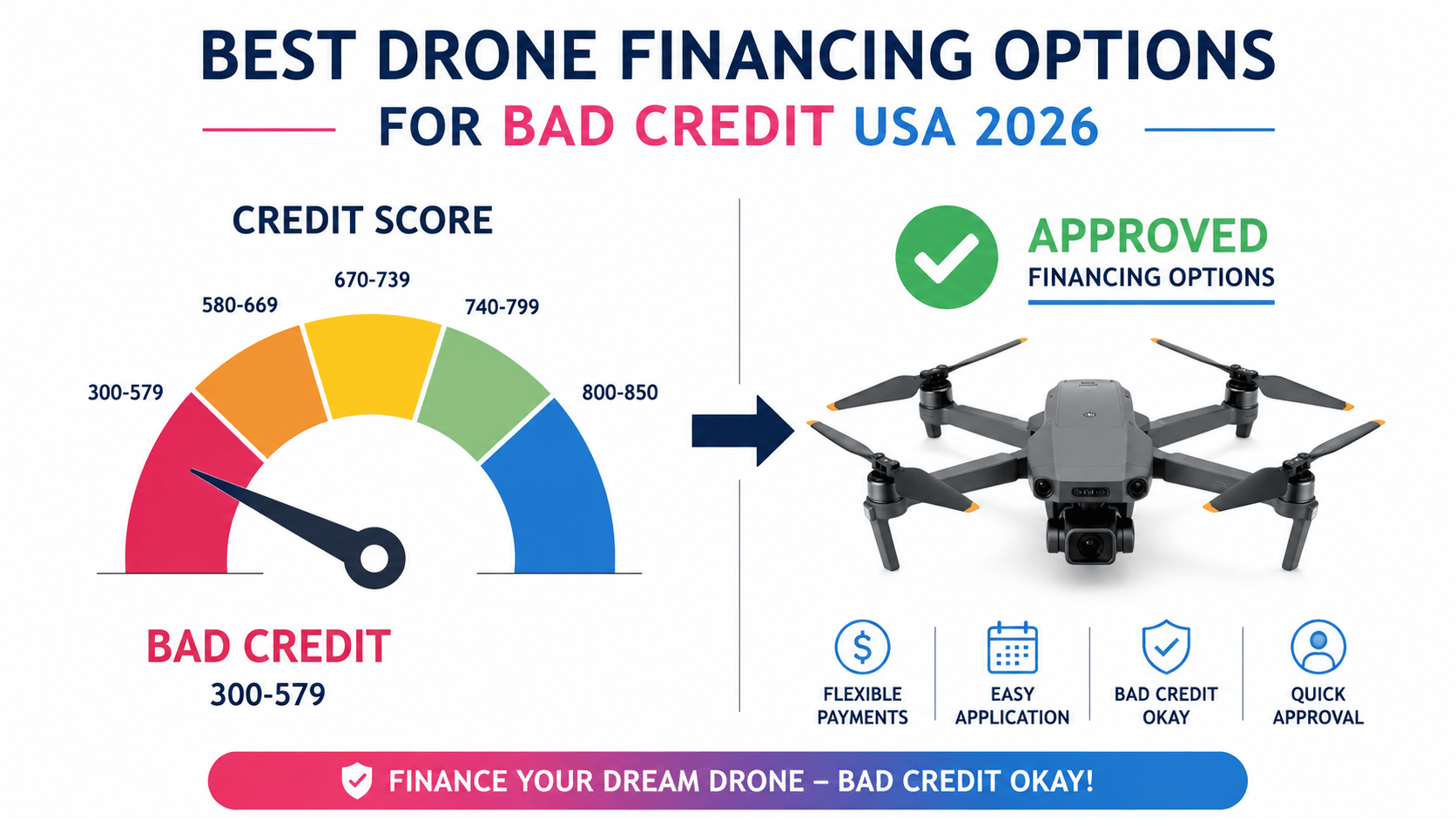

What Counts as Bad Credit for Drone Financing?

Before anything else, you need to know where you actually stand. Lenders in the USA use FICO scores, and here is how they generally categorize them:

- 300–579: Poor credit

- 580–669: Fair credit (often treated as “bad” by traditional lenders)

- 670–739: Good credit

- 740+: Very good to exceptional

Most traditional banks and credit unions will reject drone financing for bad credit applications below 620. Some online lenders will work with scores as low as 550. And a growing number of BNPL platforms do not check your credit score at all.

So when I say drone financing for bad credit is possible in 2026, I mean specifically for buyers in the 500–669 range. Below 500, your options narrow significantly but do not disappear entirely.

Can You Really Get Drone Financing for Bad Credit in 2026?

Yes. And here is why 2026 is actually a better year for drone financing for bad credit than most people realize.

Three things have changed the landscape:

BNPL platforms have gone mainstream. Affirm, Klarna, Afterpay, and PayPal Pay Later are now available at major USA retailers including Amazon, Best Buy, and B&H Photo. Several of these do soft credit checks only — meaning your score does not take a hit just from applying, and approval rates are significantly higher than traditional loans.

Specialty lenders have expanded. Companies like Acima, Snap Finance, and Progressive Leasing specifically target buyers with poor or limited credit history. They operate on a lease-to-own model rather than a traditional loan, which changes the approval criteria entirely.

Drone prices have dropped. In 2026, capable drones exist at every price point from $100 to $2,000+. Financing a $300–$500 drone is a very different conversation than financing a $3,000 professional rig. Smaller loan amounts mean lower risk for lenders and easier approvals for buyers seeking drone financing for bad credit.

Best Drone Financing Options for Bad Credit USA Buyers

Here are the real options I’d point someone toward in 2026, in order of accessibility. Each one handles drone financing for bad credit differently, so read carefully before you apply.

1. Affirm — Best BNPL for Bad Credit Drone Buyers

Affirm is available at Amazon, Best Buy, and B&H Photo. It uses a soft credit check, which means applying does not hurt your score.

How it works:

- Choose your drone at checkout

- Select Affirm as payment method

- Pick your repayment term (3, 6, or 12 months)

- Get an instant decision

Interest rates: 0% APR on select terms, up to 36% APR on longer terms depending on your credit profile. Learn more at Affirm.com.

Approval with bad credit: Affirm approves many applicants with scores in the 550–600 range, especially for smaller purchase amounts under $500.

Watch out for: High APR on longer payment terms. Always choose the shortest term you can afford to minimize interest costs.

2. Klarna — Best for Flexible Split Payments

Klarna’s “Pay in 4” option splits your purchase into four equal payments over six weeks with zero interest. This is the most accessible drone financing for bad credit option because Klarna’s approval criteria for Pay in 4 is the most lenient of the major BNPL platforms. See full terms at Klarna.com.

Best for: Drones priced under $400 where four equal payments are manageable.

Available at: Amazon, Best Buy, and directly through some drone brand websites.

3. Acima Credit — Best Lease-to-Own Option

Acima operates on a lease-to-own model, not a traditional loan. This means your credit score is far less important than your income and banking history — making it one of the most accessible drone financing for bad credit paths available in 2026.

Approval criteria:

- Active checking account with 90+ days history

- Regular income deposits

- No minimum credit score listed

How it works: Acima purchases the item on your behalf and you make weekly or monthly payments. You have the option to buy out the lease early, which saves significant money.

Watch out for: If you go full term without early buyout, the total cost can be 1.5x to 2x the retail price. Always aim for early buyout if you use this option.

4. Snap Finance — Best for Very Poor Credit

Snap Finance specifically markets to buyers with poor or no credit. They use income and banking data rather than credit score as the primary approval factor — a genuine drone financing for bad credit solution for scores below 550.

Available at: Select retailers. Not available directly on Amazon — check their retailer locator at SnapFinance.com.

Best for: Buyers with scores below 550 who have stable income.

Same warning as Acima: The total cost at full term is high. Treat this as an emergency option, not a first choice.

5. PayPal Pay Later — Best for Existing PayPal Users

If you already have a PayPal account in good standing, PayPal Pay Later gives you access to split payment options with minimal friction. Existing account history matters more than your credit score here.

Pay in 4: Zero interest, four payments over six weeks. Pay Monthly: Longer terms available for purchases over $199, with interest rates varying by credit profile.

Buy Now Pay Later (BNPL) for Drone Financing With Bad Credit — What You Need to Know

BNPL sounds simple but there are a few things that catch people off guard. Let me be direct about them.

Soft vs Hard Credit Checks

Most BNPL platforms do a soft check for their split-payment products (Pay in 4 style). This does not affect your credit score. However, if you apply for longer-term monthly financing through the same platform, they often run a hard check. Know which product you’re applying for before you click confirm.

Missing Payments Hurts You

BNPL platforms report missed payments to credit bureaus. If you’re already dealing with bad credit, a missed BNPL payment makes things worse. Only commit to a drone financing plan you’re certain you can maintain.

0% APR Has an Expiry

Some 0% APR offers convert to high interest rates if the balance is not paid in full by the end of the promotional period. Read the full terms before you commit. The Consumer Financial Protection Bureau has a helpful overview of BNPL rights and risks for USA buyers.

No Credit Check Drone Financing — Is It Real?

Yes, but the terminology is slightly misleading. Here is what “no credit check” actually means in the context of drone financing for bad credit.

Most platforms that advertise no credit check are doing one of two things:

- Soft check only — They check your credit but it doesn’t affect your score and their approval criteria are more flexible.

- Alternative data check — They skip the FICO score entirely and look at your bank account history, income deposits, and spending patterns instead.

True zero-check financing with no income verification is rare and almost always comes with extremely high costs. Avoid any lender promising guaranteed approval with no verification at all — that’s almost always a predatory lending trap.

I cover the full landscape of no credit check options in detail in my drone financing no credit check guide — worth reading alongside this article.

How to Improve Your Drone Financing for Bad Credit Approval Chances Fast

Even with bad credit, there are things you can do right now to improve your odds before you apply for drone financing.

Use a bank account with consistent deposits. BNPL platforms and alternative lenders look at cash flow. Regular deposits signal stability even when your credit score doesn’t.

Apply for smaller amounts first. A $200 drone is easier to finance than a $1,200 drone. Start with what you can realistically get approved for, build a payment history, and upgrade later.

Avoid applying to multiple lenders at once. Every hard inquiry drops your score slightly. Space out applications and start with soft-check platforms.

Consider a secured credit card. If you have time before you need the drone, a secured card used responsibly for 3–6 months can move your score meaningfully. This is a longer play but worth mentioning.

Have your income documentation ready. Pay stubs, bank statements, or proof of self-employment income all help with alternative lenders. The faster you can verify income, the smoother the drone financing for bad credit process becomes.

What Drone Should You Finance With Bad Credit?

This matters more than most people think. Financing a $1,500 drone with bad credit and high-interest terms is a bad financial decision even if you get approved. Here is how I’d think about drone financing for bad credit by price range.

Under $300: Pay outright if at all possible. Financing this range on high interest costs more than the drone is worth.

$300–$600: BNPL Pay in 4 with zero interest is the ideal drone financing for bad credit option here. Manageable payments, zero interest, short term.

$600–$1,500: Use Affirm or PayPal Pay Monthly only if you have a clear income plan to cover payments. This range makes sense for business use.

Over $1,500: If your credit is genuinely poor, I’d wait and save rather than finance at high interest. The total cost difference is significant.

For drones in the $300–$600 range that make sense to finance, check my guides on best drones under $500 and best drones under $300 — both cover solid options at price points that make drone financing for bad credit practical.

If you’re starting smaller, my best drones under $200 guide covers the most accessible end of the market where paying outright is usually the smarter move.

One More Thing Before You Use Drone Financing for Bad Credit

Once you have your drone, two things matter immediately: knowing the rules and protecting yourself.

Flying without understanding the regulations is a fast way to get fined. My drone laws in USA guide covers what every USA buyer needs to know before their first flight. You can also check current airspace restrictions directly on the FAA DroneZone before every flight.

And if you’re using a financed drone for any kind of business purpose, insurance is not optional. A single incident without coverage can cost far more than the drone itself. My drone insurance for business guide breaks down exactly what coverage you need and what it costs in 2026.

FAQ: Drone Financing for Bad Credit in 2026

Drone Financing for Bad Credit — FAQ

Honest answers for USA buyers in 2026

Financing Questions

Yes. Drone financing for bad credit is possible through BNPL platforms like Affirm and Klarna, and lease-to-own services like Acima and Snap Finance. Your income and banking history matter more than your FICO score with these lenders.

Traditional lenders typically require 620+. BNPL platforms like Affirm work with scores as low as 550. Lease-to-own services like Acima and Snap Finance have no stated minimum credit score requirement.

Most BNPL platforms use soft credit checks only, which do not affect your score. Longer-term monthly financing options often involve a hard check. Always confirm before applying.

Mostly yes. Most “no credit check” lenders use alternative data — your bank account history and income — instead of your FICO score. True no-verification financing is rare and usually comes with predatory terms. Avoid guaranteed approval offers with no verification required.

Klarna Pay in 4 is the most accessible for bad credit buyers — zero interest, four payments over six weeks, soft check only. Affirm is the best option for larger purchases where you need more than six weeks to pay.

For drones under $300, saving and buying outright is almost always the better financial decision. Use drone financing for bad credit only when you can access 0% APR terms or when the drone will generate income.

Insurance Questions

It is not legally required for recreational flying, but it is strongly recommended. If you crash a financed drone, you still owe the remaining payments. Insurance protects your investment and your liability.

Recreational liability coverage starts around $75–$100 per year. On-demand coverage runs $10–$15 per flight day. See the full breakdown at the drone insurance cost guide 2026.

Buying Questions

Start with a drone in the $150–$300 range where Klarna Pay in 4 covers the full amount interest-free. The DJI Mini 2 SE and Holy Stone HS720E are solid options. Avoid financing anything over $500 until your credit improves.

For recreational flying with drones under 250g, no FAA license is required. For commercial use — selling footage, client work — you need a Part 107 license regardless of drone price or how you paid for it.

More drone financing guides at HitnBuy.com

Final Thoughts: Drone Financing for Bad Credit in 2026 Is More Accessible Than You Think

Here is the honest summary.

Drone financing for bad credit in 2026 is genuinely possible for most USA buyers. The key is matching the right financing tool to your situation — BNPL for smaller purchases, lease-to-own for buyers with very poor credit, and alternative lenders for those who need more flexibility than traditional banks offer.

What I’d tell anyone pursuing drone financing for bad credit: start small, use 0% interest options wherever possible, and treat financing as a tool for income-generating purchases rather than hobby spending. A financed drone that pays for itself through client work is a smart move. A financed toy drone at 30% APR is not.

If you haven’t already read my full drone financing guide 2026, that’s your next stop — it covers every financing path available to USA buyers across all credit levels in one place.

And if you’re ready to pick the drone itself, my best budget drones for beginners guide will help you find the right model at the right price before you commit to any payment plan.

Drone financing for bad credit in 2026 is not the obstacle it used to be. You just need to know the right doors to knock on.